wildpixel/iStock via Getty Images

Sportradar Group AG (NASDAQ:SRAD) is a Rule of 40 company trading at 12x NTM EBITDA. In other words, they are the leading provider of B2B technology solutions in the sports betting industry, boasting a ~20% adjusted EBITDA margin and over 20% revenue growth. The company has secured most of the exclusive contracts with major sports leagues, their revenue is primarily subscription-driven (~80%), and they have one of the best management teams in the industry. In this piece, I’ll explain why SRAD stock trades at a discount but remains undervalued.

Company and Situation Overview

Sportradar Group AG offers sports data services for the betting and media industries in over 115 countries. Operating under the Betradar and Sportradar Media Services brands, it provides mission-critical software, data, and content to over 1,800 customers including 350+ sports leagues, ~1,000 betting operators, and 500+ media companies. The company supports the entire sports betting process, from data collection to risk management, and was founded in 2001 with headquarters in St. Gallen, Switzerland. The company IPO’d in 2021 through a SPAC and employs ~4,000 individuals.

4Q FY23 Earnings Call Presentation

In terms of ownership, Sportradar is currently held by management and public investors, with management owning about 44% of the company and public investors owning 56%. The company’s founder and CEO, Carsten Koerl, holds a substantial 31.6% stake in the company and wields nearly 82% of the voting power. Other significant shareholders include the Canada Pension Plan, which holds a 26.8% stake, TMCI, which owns 11.5%, and Radcliff, which holds 5.1%. Together, management and the top three public shareholders control 87.1% of Sportradar’s equity value and almost all of the voting power.

Sportradar Has an Economic Moat

1.0 Global Market Leader in a Concentrated Market

Sportradar 2021 IPO Deck

Sportradar holds a dominant position in the global sports betting industry, a $10 billion industry. With approximately 60% market share globally, Sportradar stands as the number one provider of B2B technology solutions in this space. Its closest competitors include Genius Sports (GENI), which has a ~25% market share, and Stats Perform, owned by Vista Equity Partners, which holds less than 15% market share. In the US, Sportradar’s dominance is even more pronounced, supplying data to over 85% of all bookmakers, with 90% of its customers on a subscription plus revenue share model.

2.0 High Barriers to Entry and Exit

Sportradar 2021 IPO Deck

Sportradar’s moat is fortified by exclusive contracts with premier U.S. leagues like the NHL, NBA, and MLB (outside of the US), as well as international leagues and federations such as FIFA, Bundesliga, and ITF. These exclusive relationships form a significant barrier for competitors. The company’s mission-critical product portfolio is integral to B2C success, and the high switching costs deter customers from leaving. Also, Sportradar’s deep operational and technological integration with its customers further solidifies its position, creating both high barriers to entry for competitors and high barriers to exit for clients.

3.0 Strong, Recurring, Predictable, and Diversified Cash Flows

Author’s Data

Author’s Data

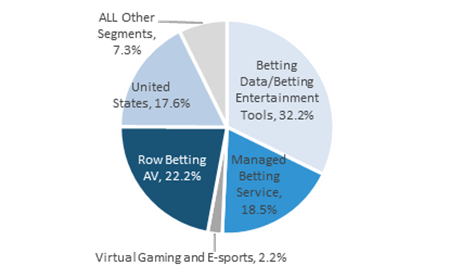

One of Sportradar’s greatest strengths is its subscription model and revenue-sharing agreements, which provide a highly visible and recurring revenue base. About 80% of the company’s revenue is subscription-driven, with opportunities for upside through increased betting volume growth. The diversified revenue base, achieved through cross-selling data-rights with managed-betting, audio-visual, and marketing services, operates at high margins due to significant operating leverage. The company’s impressive net dollar retention rate of 120%, average customer tenure of 10 years, and revenue churn of only 0.6% further highlight the predictability of its cash flows.

4.0 Strong Management Team

Sportradar 2021 IPO Deck

Sportradar’s management team, in my view, is unparalleled in the industry, with each executive boasting over 30 years of relevant industry experience. The team includes veterans from prestigious organizations like EQT, ESPN, UEFA, Fiserv, Worldpay, BBG, and CPP, which provides a solid foundation for the company’s strategic direction and operational excellence.

5.0 Fast-Growing Business and Industry

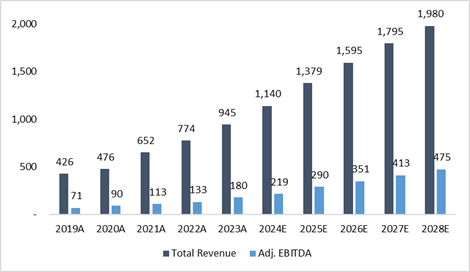

The sports betting industry, particularly in the US, is one of the fastest-growing segments within the gaming market. US sports betting has surged from $1.7 billion in 2019 to $8 billion in 2022, representing a compound annual growth rate (“CAGR”) of 68%. By 2027, the market is expected to reach $17.4 billion, growing at a CAGR of 17%. Globally, sports betting is projected to grow from $65 billion in 2022 to $103.5 billion in 2027, with a CAGR of 9.8%. Sportradar has doubled its revenue and EBITDA from 2019 to 2023, and is on track to double its EBITDA again by 2027, which underscores the company’s rapid growth trajectory.

6.0 Proven Acquisition Platform

Sportradar 2021 IPO Deck

Sportradar has a strong track record of successful acquisitions, with 15 tuck-in acquisitions to date and a robust M&A pipeline, averaging one add-on per year since 2010. This demonstrates the company’s superior capital allocation and integration strategy, contributing to a 24% revenue CAGR from 2019 to 2022.

Investment Thesis

Sportradar is the leading global B2B platform providing essential data and services to the sports betting industry. The company is particularly well-positioned to capture a growing share of the US betting market, which is experiencing radical growth. The management team expects double-digit revenue CAGR through the end of the decade, driven by market growth, new markets, new products, and increased product penetration and I believe it is feasible given Sportradar’s dominant position in this fast-growing sports betting industry. Additionally, I believe EBITDA margins are likely to increase from 20% to 25% as Sportradar continues to scale in the US.

Overall, I believe Sportradar offers investors interested in long-term exposure to the rapidly growing sports betting industry a pure-play opportunity through a profitable, majority subscription-based (~80% of revenue), B2B operating model. The company has one of the strongest growth profiles in its sector, with a 20% two-year adjusted EBITDA CAGR, a strong balance sheet (i.e., $240M more in cash than debt, and 98% equity as % of total capital), $200M in planned share repurchases for 2024, increased operating leverage in future years, and a reasonable valuation considering its growth prospects and comparable companies.

The latest conference call was the most confident and concise messaging from management that I’ve heard since the company’s IPO in September 2021. The focus wasn’t on the fact that Sportradar crushed street expectations, but rather on the positive tone in their guidance. For example, the 2024 revenue guidance of “at least 20% growth” improved from the previous quarter’s “+/-20%”. Management also noted that this business, even without future rights agreements, can maintain attractive growth rates, following 20% growth in 2023 and 30% in 2022.

Sportradar’s structural advantages continue to expand, its fundamentals are set to accelerate, and I think the stock at 12x EV/EBITDA is highly attractive, especially for a Rule of 40 company. The company has multiple revenue tailwinds, including online sports betting volume growth, in-play mix shift, increasing take rate, and market share gains, alongside high incremental margins due to its mostly fixed cost structure.

In 2024, there will be a margin headwind of ~500 basis points from new rights deals with ATP/NBA, but an equivalent amount of improvement on operating costs excluding rights. This points to a compelling P&L acceleration starting in 2025 and continuing for many years beyond. In my view, now is the time to buy the stock before its strong performance becomes obvious in the reported financials.

Valuation

Comparable Companies

For those that don’t know what Rule of 40 means, it is a ratio for Software as a Service (SaaS) companies that combines the revenue growth rate and profit margin, and states that it should equal or exceed 40%. Companies above 40% are generally generating profit at a sustained rate, while companies below 40% may face cash flow or liquidity issues. In 2023, SRAD grew 22.1% in revenue and reported a 19% adj. EBITDA margin, marking it 100bps over the Rule of 40.

Since Genius Sports is the only comparable company, I compare Sportradar to other Data Providers other SaaS companies that meet the Rule of 40 criteria:

Author’s Data

As shown in the figure above, Sportradar’s valuation doesn’t make sense. However, as mentioned earlier, Sportradar only has a ~56% float on their public shares. Thus, they are less liquid than the comps, giving them a liquidity discount on their valuation. Nonetheless, I don’t believe SRAD should be trading at 12x 2025 adj. EBITDA. Thus, I’ve provided a discounted cash flows analysis to find its intrinsic value below.

Discounted Cash Flows Analysis

Below is a summary of the operating model and discounted cash flow analysis I constructed using the Bloomberg Consensus Street estimates. The model shows that Sportradar is experiencing rapid growth while maintaining approximately an 80% gross margin and a 20% adjusted EBITDA margin. The main factor reducing Sportradar’s cash flows isn’t reflected on the income statement but on the cash flow statement, specifically under Capex. This includes the acquisition of sports rights, where in 2023, Sportradar allocated about $200 million to rights acquisitions and the remainder to purchases of PPE. Despite this, the high Capex leads to significant D&A expenses, which in turn provide a tax benefit that helps improve the cash flows.

Author’s Data

Author’s Data

As shown above, I’ve set a price target of $12 using a 16x exit multiple, which aligns with the current trading value, and a 17.22% cost of capital, which includes a 2% firm-specific risk premium due to liquidity. This represents a 31% premium over today’s prices, which I still consider conservative given Sportradar is a Rule of 40 company.

I believe this is a good way to value Sportradar for a couple of reasons. First, the cost of capital is an input that represents the risks of a company’s cash flows. Typically, the cost of capital ranges from 8% to 12% for the average company. Sportradar’s cost of capital is slightly above 15%. However, I increased it to 17.2% to account for additional risk in their cash flows, aiming to be conservative. If you are more conservative in your valuation and the company still yields an attractive intrinsic value, there is less risk in investing today, given the potential reward. In other words, if the cost of capital (also known as the discount rate or expected return) is 17% (quite high) and the company is still undervalued, that signals an undervalued company. Second, there are no good comps or precedent transactions comparable to Sportradar, other than GENI, making a relative valuation inaccurate.

Risks to Rating and Price Target

1.0 Geopolitical Risk – SRAD has exposure in regions like Ukraine and Russia for data aggregation and monetization. Any instability or conflict in these areas could disrupt the operations and impact performance.

2.0 Rights Cost – If SRAD cannot pass along the increasing fees that leagues may demand for official rights to its clients, it would negatively impact its financials. Also, potential infringement issues related to these rights is a risk to keep in mind.

3.0 Competition – Competition for official sports rights is intense, and increased competition would negatively affect SRAD’s ROI and overall economics. This heightened competition would lead to inflated costs for acquiring these rights or reduced profitability from ventures.

4.0 Ownership of Data and Project Red Card – Project Red Card is where former members of the English Premier League have submitted a data subject access request under the GDPR in the UK. They seek compensation for performance data that third parties, such as Sportradar, profit from. While this has not yet turned into a legal claim, and precedent suggests such data is public fact, an unfavorable ruling would significantly impact Sportradar’s economics of sports data distribution.

5.0 Acquisitions – SRAD has a history of multiple acquisitions. The risk here lies in SRAD’s ability to properly integrate these acquired businesses and realize synergies.

Bottom Line

Through my research and understanding, I don’t see how Sportradar’s business model could be significantly improved. With its dominant market position, best-in-class financials, strong management team, predictability, and high growth, the company has significantly stood out to me. While the stock may trade discounted due to liquidity, its intrinsic value and potential for future growth make it the most attractive investment for investors seeking long-term exposure to this space.

If there is anything you believe I missed, please leave a comment below.